One of the most common misconceptions among first-time buyers in Nagpur is that you cannot get a bank loan to purchase a plot. This is simply not true. Banks and housing finance companies do offer loans for plot purchases - but the rules, eligibility criteria, and documentation requirements are somewhat different from a standard home loan.

If you are planning to buy a residential plot in Nagpur and want to understand how plot financing works, this guide covers everything you need to know - from the types of loans available to the documents you will need to the interest rate landscape in 2026.

Can You Actually Get a Loan for a Plot?

Yes, absolutely. Most nationalised banks - including State Bank of India, Bank of Baroda, and Punjab National Bank - as well as private banks like HDFC, ICICI, and Axis Bank offer loans specifically for residential plot purchases. Housing finance companies like LIC Housing Finance and PNB Housing also offer plot loans.

However, there is an important condition: the plot must be within an approved residential layout. In Nagpur's context, this means the plot should be in an NMRDA or NIT-sanctioned layout. Banks will not finance plots on agricultural land, plots without clear title, or unapproved layouts. This is yet another reason why buying a sanctioned plot matters so much.

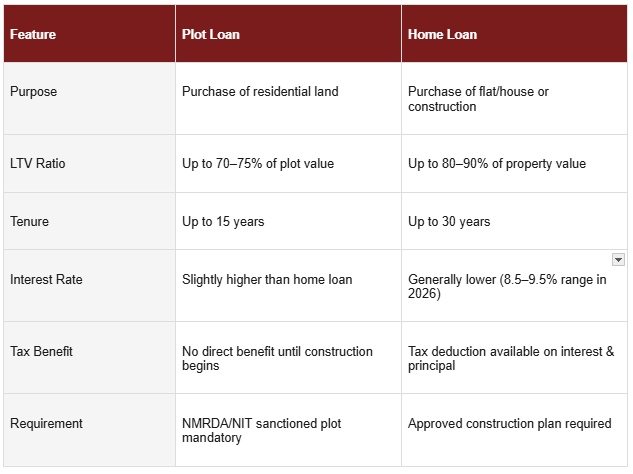

Plot Loan vs Home Loan: What is the Difference?

| Many buyers confuse a plot loan with a home loan. They are related — but not the same. Understanding the difference helps you plan your finances correctly. |

How Much Loan Can You Get?

Most banks offer a plot loan of up to 70 to 75 percent of the plot's market value or the registered sale value — whichever is lower. This means if you are purchasing a plot worth Rs. 20 lakhs, you could potentially borrow up to Rs. 14 to 15 lakhs, and you would need to arrange the remaining Rs. 5 to 6 lakhs as a down payment from your own funds.

Some banks may offer higher LTV ratios for applicants with strong credit profiles, stable income, and existing banking relationships. The exact amount will depend on your income, existing liabilities, and the bank's internal assessment.

Documents Required for a Plot Loan in Nagpur

Having your documents in order significantly speeds up the loan approval process. Here is a standard checklist:

Personal Documents

• Identity proof: Aadhaar card, PAN card, passport, or voter ID

• Address proof: Aadhaar, utility bill, or bank statement

• Income proof: last 3 months' salary slips (salaried), or last 2 years' IT returns with computation (self-employed)

• Bank statements: last 6 months

• Employment proof: offer letter, employment certificate, or business registration

• Passport-size photographs

Property Documents

• Sale agreement or allotment letter from the developer

• Sanctioned layout plan from NMRDA or NIT

• 7/12 extract (Satbara Utara) of the land

• Property card (for urban land)

• Encumbrance certificate - to confirm no existing loans or disputes on the property

• Title deed or chain of ownership documents

• NOC from the developer (if applicable)

• Copy of the registered development agreement

| Mahalaxmi Group provides complete documentation support to every buyer. Our team coordinates directly with your bank, prepares the required property documents, and ensures the entire process moves smoothly from application to disbursement. |

The Loan Process: Step by Step

1. Application: Submit your loan application with personal and property documents to your chosen bank.

2. Property Verification: The bank sends its legal and technical team to verify the plot — title, NMRDA sanction, and physical boundaries.

3. Credit Assessment: The bank evaluates your income, credit score, and existing EMIs to determine eligibility and loan amount.

4. Sanction Letter: If approved, the bank issues a formal sanction letter stating the loan amount, tenure, interest rate, and conditions.

5. Disbursement: Once the sale deed is registered and stamp duty is paid, the bank releases the loan amount directly to the seller.

Which Banks Work with Mahalaxmi Group?

Mahalaxmi Group has established working relationships with several nationalised and private banks for plot loan financing across our projects. This means our team can help you get pre-assessed, coordinate document submission, and in many cases, expedite approvals compared to approaching a bank cold.

Our tie-ups cover both plot loans for land purchase and composite loans for buyers who want to purchase a plot and construct a home in a combined loan product. Our advisors can help you identify which bank and product best suits your income profile and repayment capacity.

Tips for Getting Your Plot Loan Approved Faster

• Maintain a credit score of 750 or above - this is the threshold most banks look for.

• Reduce existing EMI obligations before applying - banks use a FOIR (Fixed Obligation to Income Ratio) of typically 40–50%.

• Keep your bank statements clean for 6 months prior to application - avoid large unexplained withdrawals or deposits.

• Choose an NMRDA-sanctioned plot - this is non-negotiable for loan approval.

• Work with a developer who has bank tie-ups - the pre-approved project status significantly reduces processing time.

A Final Word on Financing Your Dream Plot

Buying a plot in Nagpur does not have to be an all-cash decision. With the right planning, documentation, and a trusted developer who understands the financing ecosystem, getting a plot loan in Nagpur is a straightforward process.

The key is starting with a legally sound, NMRDA-approved property and working with people who have done this many times before. At Mahalaxmi Group, we have helped thousands of buyers navigate the loan process successfully - and we are ready to help you too.

| We have tie-ups with leading nationalised and private banks. Let us help you get your plot loan approved. Reach out at mahalaxmiinfra.in or visit our office today. |

Ready to Take the Next Step?

— Published by Mahalaxmi Group, Nagpur · mahalaxmiinfra.in